Credit risk performance update - March 2022

Today we published our Q1 2022 performance update on our statistics page, and this blog piece is also our Outcome Statement for 2021.

In Q1 2022, we focused on understanding the impact of cost-of-living challenges on our active loan customers and how we can support those who may see their financial circumstances being impacted.

Both expected annual returns and expected annual loss rates have remained stable compared to our Q4 2021 update.

We are also pleased to inform you that the interest rate diversion to the Shield will be reduced for the 2019 cohort. However, it will continue to be applied to 2018 and earlier cohorts. The 2020 and 2021 cohorts will continue to pay the target interest rate.

Expected annual returns

Both expected annual returns and expected annual loss rates have remained stable compared to our Q4 2021 update.

Expected annual losses have been updated to reflect the most recent portfolio performance and the results of our stress testing. We will continue to understand the impact of the cost-of-living challenges on the economy, UK consumers and our active loan customers.

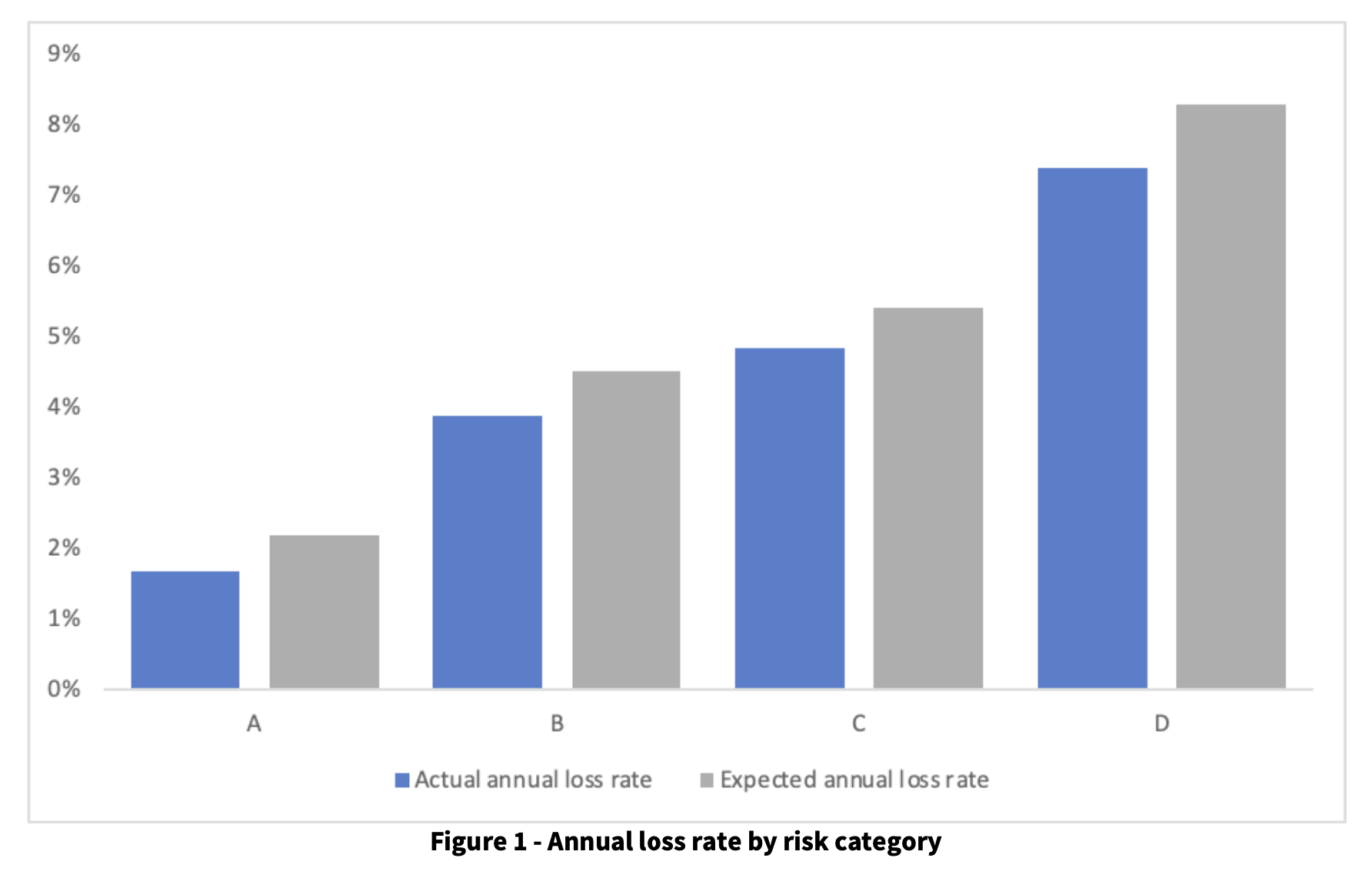

Overall expected annual losses on the active portfolio remained relatively stable at 4.1% in Q1 2021, compared to approximately 4% in Q4 2021. However, we anticipate a potential further increase in loss rates in the short-medium term. We expect some of our loan customers to fall into financial distress as the cost-of-living increases, so we will closely monitor this.

Figure 1 below shows our latest expected annual loss rate, by risk category, compared to the actual loss rate incurred to date.

Expected annual returns have remained relatively stable and broadly aligned with the Q4 2021 performance update.

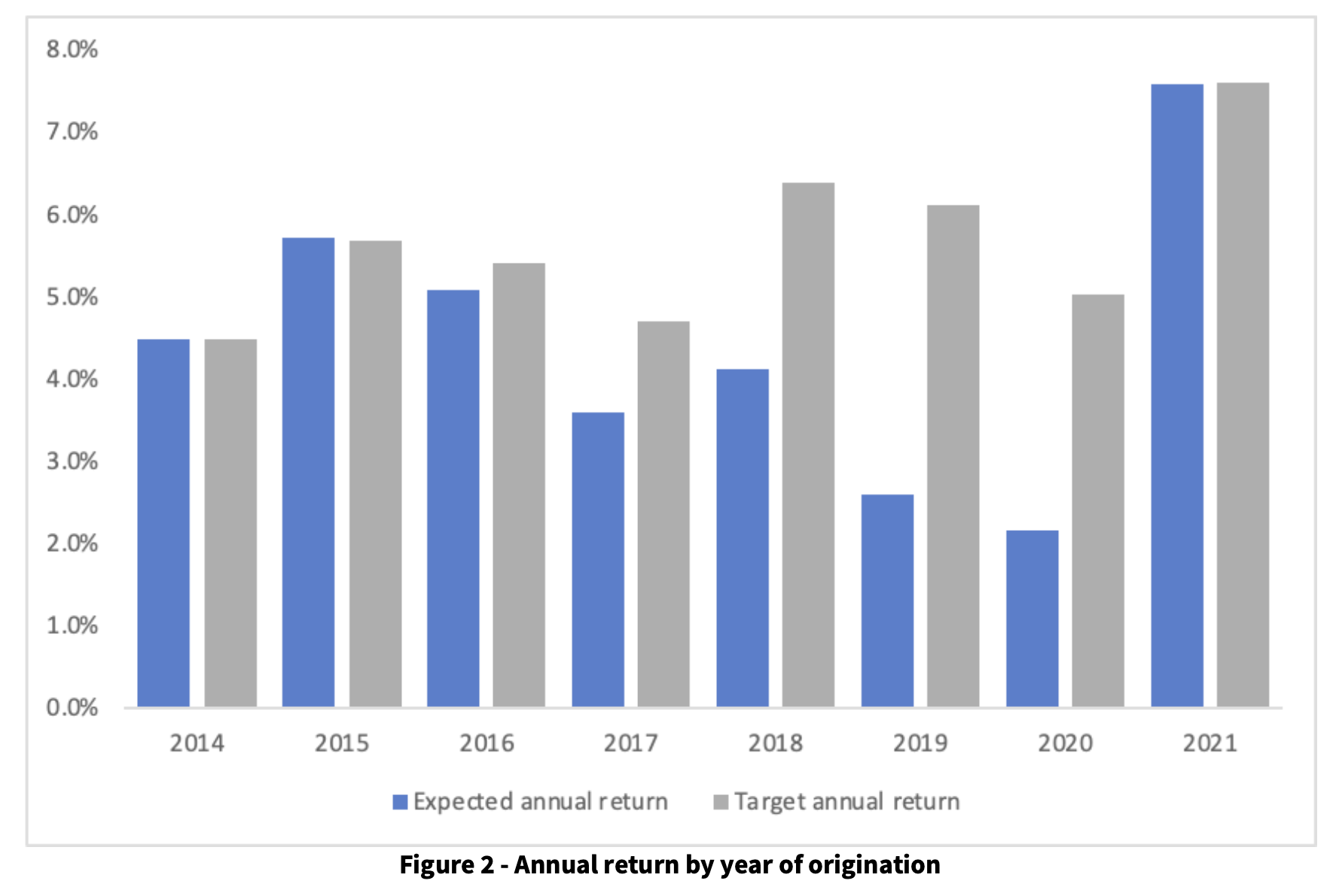

Average returns on past cohorts (2014-2019) are 4.4% p.a. for Growth investments and 3.8% p.a. for Flexible.

The 2020 and 2021 cohorts' average returns are 2.6% p.a. and 4.5% p.a. for Growth and 1.9% and 4.0%p.a. for Flexible, respectively, which are stable compared to the Q4 2021 performance update.

We are pleased to inform you that the interest rate diversion to the Shield will be reduced for the 2019 cohort. However, it will continue to be applied to 2018 and earlier cohorts. The 2020 and 2021 cohorts will continue to pay the target interest rate.

Finally, figure 2 below shows our latest expected annual return, by year of origination, compared to the annual target return when the investment was made.

Whilst 2017-2020 cohorts have decreased compared to their annual target return; returns remain positive at approximately 3.1% p.a. on average.

The Lending Works Shield

The future income required to cover expected losses decreased to £1.5m, compared to £2.2m in Q4 2021. The £1.5m reflects the most recent performance of the portfolio and our latest assessment of the expected credit losses in our portfolio as it matures.

The Shield cash balance has remained relatively stable at £1.1m in Q1 2022. Shield cash utilisation continues to be maximised to pay arrears and default to retail investors.

Next update

Our next statistics page update will be in July 2022, and it will continue to be focused on the impact of cost-of-living could have on the Lending Works' portfolio performance.